Last verified: June 2026. Written by Dinh Minh Vu (M.Sc. Computer Science, University of Passau), based on about 8 months of personal use as a Vietnamese working student banking with bunq in Germany, plus bunq's official help center documentation. This is personal experience and general information, not financial advice. Always check bunq's current plans and terms before signing up.

Short answer: yes, bunq is legit, and yes, it is a good bank account for students in Germany. It is also the account I actually use to receive my Werkstudent salary every month. I switched to it after N26 rejected my Vietnamese passport and Commerzbank turned me away in person, twice. Eight months later, it is still the account I recommend first to other international students, with a few honest caveats below.

Open a bunq account here* if you want to follow along, or keep reading for the full picture, including the parts that did not work for me.

Quick verdict before the details:

Legit and regulated. bunq operates under a Dutch banking license from De Nederlandsche Bank, with a registered German branch in Cologne supervised cross-border by BaFin. Deposits are protected up to €100,000 under the Dutch Deposit Guarantee Scheme.

Fast, app-based signup. Verification took minutes, fully in the app, with just my passport. No Anmeldung or Steuer-ID needed to open the account.

German IBAN for salary, rent, and direct debits.

Free for students. bunq Pro, normally €9.99/month, is 100% free once you upload proof of enrollment.

The downsides. No real credit card, not supported by Apple's German installment financing partner, and it is not a brokerage. I now keep most of my investing elsewhere.

My situation: why I needed bunq in the first place

I am Vietnamese, and I came to Germany to study at the University of Passau. Before bunq, I tried the obvious options and ran into walls everywhere.

N26 was my first choice, since it is the best-known free neobank for students. It did not work out, because N26 does not accept Vietnamese passports. The accepted-documents list requires a residence permit card for many nationalities, including mine, and applying for that card from scratch takes far too long when you need a working bank account now.

Deutsche Bank and Sparkasse are solid traditional banks, but their apps and account-opening flows are heavily in German. At the time, my German was around A2, and trying to open an account in a language I barely understood was stressful and slow.

Commerzbank refused me twice in person. The first time, because I did not yet have a Steuer-ID (it arrives by post after your Anmeldung). The second time, they told me there was a system error and they could not create a student account for me at all. I might have just been unlucky, but two failed in-person visits were enough.

I generally prefer online banks anyway, so I do not have to explain my situation to a representative across a desk in a language I am still learning. bunq solved this completely: I opened the account from my phone with just my passport, and it worked the first time.

If a similar situation sounds familiar, I also wrote a more detailed bank account guide for Vietnamese students in Germany covering more options and the document requirements for each.

Is bunq legit and safe?

This is the question I get asked most, so let me be precise about it.

bunq is not a German bank. It is a Dutch bank, bunq B.V., holding a full banking license issued by De Nederlandsche Bank (the Dutch central bank). In Germany, it operates through a registered branch, bunq B.V. Niederlassung Deutschland, based in Cologne, which is registered with BaFin as a cross-border EEA branch. This is a completely normal and legal setup under EU banking passporting rules, the same framework many other European neobanks use.

The part that matters most for "is my money safe" is deposit protection. Your bunq balance is covered by the Dutch Deposit Guarantee Scheme (DGS) up to €100,000 per person, the same €100,000 ceiling as the German scheme, just administered by Dutch authorities (De Nederlandsche Bank) instead of German ones. If bunq ever became unable to meet its obligations, this is the scheme that would pay you out.

So: legit, regulated, and your deposits are protected, just under Dutch rather than German supervision. For me, that distinction never mattered in practice, but it is worth knowing exactly what "safe" means here instead of taking it on faith.

Signing up as a student: what you actually need

This was the easiest part of the entire process. Here is what I needed, and what I did not need:

Passport: required for identity verification. I used my Vietnamese passport.

Visa or residence permit: not required to open the account.

Anmeldung (address registration): not required upfront. I added my German address later, once I had it.

Steuer-ID: not required upfront either. Mine arrived by post a few weeks after my Anmeldung, and I added it to bunq afterwards.

Verification itself was fast, app-based, and I do not remember waiting more than a few minutes. No video call, no branch visit.

The one thing Anmeldung unlocked later was access to certain features, in my case stock trading inside the app. When I wanted to use that, I uploaded my Anmeldung confirmation through bunq's support chat, and it was approved within a day.

If you want the full picture of what is and is not possible before you have a registered address, our guide on opening a German bank account without Anmeldung goes through this in more detail across several banks.

bunq Pro free for students (and Elite at 50% off)

This is the detail that makes bunq genuinely cheap for students, and it is easy to miss if you do not look for it.

bunq's paid plans for 2026 are bunq Free, bunq Core, bunq Pro (€9.99/month), and bunq Elite (€18.99/month). I am on bunq Pro, and I pay nothing for it.

Here is how the student discount works:

If you are a university student, you can upload proof of enrollment (an Immatrikulationsbescheinigung works fine) through bunq's in-app support chat.

Once verified, bunq Pro becomes 100% free, and the discount applies immediately, not at the start of next month.

bunq Elite gets a 50% discount instead (around €9/month instead of €18.99), if you want the higher-tier plan.

bunq re-checks your student status roughly once a year, so keep an updated enrollment certificate handy when it asks again.

I uploaded my Immatrikulationsbescheinigung from the University of Passau student portal, and the AI support agent verified it almost immediately (more on that below). You can check current plan pricing and the student offer here* before signing up, since bunq does occasionally adjust plan details.

Getting paid: salary, rent, and direct debits

The whole point of switching banks was to have a working account for my Werkstudent salary, and on this front bunq has been completely uneventful, in a good way.

Salary: I have received my working student salary into my bunq account every month for 8 months, with no delays or issues.

SEPA direct debits (Lastschrift): my monthly health insurance payment to TK (Techniker Krankenkasse) and my internet bill from Telepark Passau are both set up as direct debits from bunq, and both work exactly like they would from a German bank, because the account has a German DE IBAN.

If you are setting up your finances for your first paycheck, our first salary checklist for working students walks through everything you need in place before payday, including the bank account step. And if health insurance is still an open question for you, see our health insurance guide for working students in Germany.

Fees: what I actually pay

Foreign currency payments: no extra fee from bunq. Card payments in other currencies get converted automatically at the market rate.

Cash withdrawals: I have never used the bunq card directly at an ATM. Instead, I use bunq's in-app cash withdrawal feature, which generates a QR code you scan at supported retail locations like REWE or Rossmann to get cash from the till. It works well and I have not paid anything extra for it.

Features I actually use

A few things that have genuinely become part of my routine:

Sub-accounts. I keep a separate sub-account just for the running costs of this website (workingstudentjobs.de): hosting, domain renewal, and similar small recurring charges. Having that money physically separated from my everyday spending account makes it much easier to see at a glance whether my "business" costs are covered, without doing any manual budgeting.

Apple Pay and cards. Apple Pay works perfectly with bunq's debit, "credit", and virtual cards. One thing worth explaining clearly: bunq does not offer a real credit card the way traditional banks do. The "credit" card is still backed by your own balance, the bank is not lending you anything. The "credit" branding mainly exists so the card works at merchants and online checkouts that specifically require a credit card rather than a debit card. I also have the metal card, which looks genuinely premium and feels great to hold, but honestly I rarely use it day to day since Apple Pay covers almost everything.

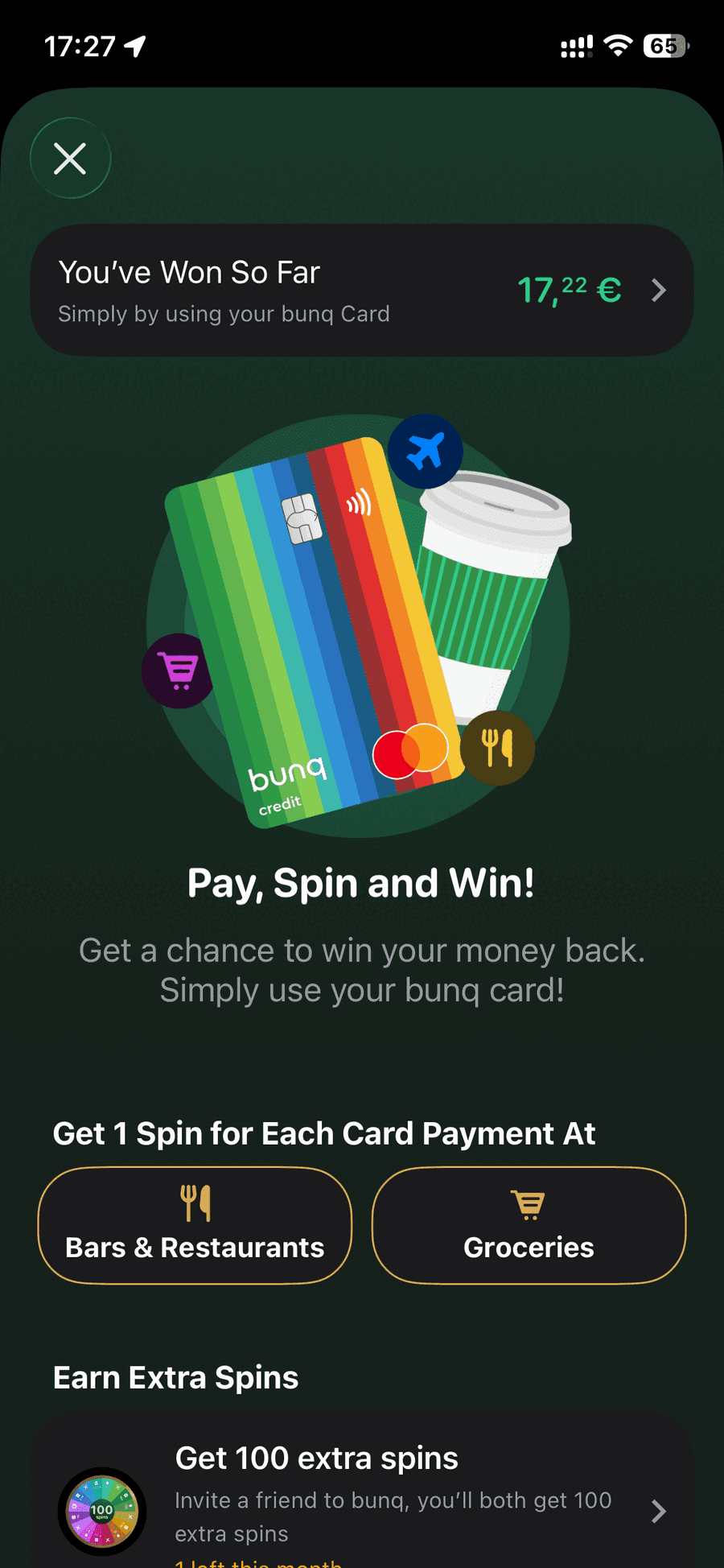

The Wheel of Fortune. bunq's reward feature (the in-app spin-to-win game, basically a lucky wheel) launched in February 2026, so I have only had it for around 4 to 5 months, not the full 8. Every time you pay with your card in certain categories (groceries, bars, restaurants on Core/Pro), you get a spin, and you can win a multiple of that payment back, sometimes 0.1x, sometimes as little as 0.01x. Over those 4 to 5 months, my total winnings add up to €17.22. It is a small, fun bonus, not something to bank on (pun intended), but it is real money I would not otherwise have had.

Savings, and why I moved my investing to Scalable Capital

bunq also pays interest on your account balance, around 3.01% per year, paid weekly, as of 2026 (bunq sometimes runs higher promotional rates for new customers in Germany for the first few months). I used this for a while and it was a nice, no-effort way to earn a bit on money sitting in my account.

Over time, though, I wanted to actually invest, not just hold cash, specifically to buy ETFs. bunq is a bank, not a brokerage, so I opened an account with Scalable Capital instead. Scalable currently pays around 2.5% per year on uninvested cash through its overnight account, on top of giving me access to the ETFs I actually wanted to buy. So far I am up more than €400 in profit there. I will cover my Scalable Capital setup properly in a separate post, since it deserves its own write-up.

For day-to-day banking (salary, rent, direct debits, spending), bunq remains my main account. For investing, Scalable Capital took over that role.

Customer support

bunq's in-app support starts with an AI assistant, and in my experience it is genuinely good, noticeably better than most "AI support" I have dealt with elsewhere. When I uploaded my Immatrikulationsbescheinigung to activate the free bunq Pro student plan, it verified the document and applied the discount quickly without me needing to escalate.

For things the AI cannot resolve, it hands off to a human agent, with a stated response time of 12 to 24 hours. I used this once, to upload my Anmeldung confirmation and unlock stock trading, and it was approved within that window without any back and forth.

The honest downsides

bunq has been good to me, but it is not perfect, and these are the two things that actually affect my day-to-day decisions:

No real credit card. As mentioned above, bunq's "credit" card is balance-backed, not a genuine line of credit. For most everyday spending this does not matter at all, but it matters the moment you need actual financing.

Not supported by Apple's German installment financing. I wanted to buy a new MacBook on installments. In Germany, Apple's financing partner for installment payments is Openbank Pay (Zinia, a Santander company), and it does not support bunq accounts. To do this, I would need a bank account from a provider Openbank Pay does support, which bunq currently is not.

This is the main reason I am planning to open a Comdirect account (the online arm of Commerzbank) once my residence permit arrives. Not because bunq failed me generally, but because this one specific use case (installment financing through Apple) needs a different bank.

bunq vs N26 vs traditional banks: the short version

If your passport or residence document is accepted by N26 and you want a fully free neobank, N26 is a reasonable alternative, our N26 vs bunq comparison for working students goes through the differences in detail, including the document acceptance question that ruled N26 out for me specifically.

If you are weighing bunq against using an international account like Wise for your salary, see our bunq vs Wise comparison, the short version is that a German DE IBAN matters more than people expect once payroll, rent, and Lastschrift forms get involved.

For a broader comparison across bunq, N26, Revolut, DKB, C24, ING, and Commerzbank, our full bank account guide for working students in Germany covers all of them side by side. To see what typical Werkstudent gross pay looks like by city and field before you estimate how much lands in your account, check our working student salary guide.

My verdict: is bunq good for students in Germany?

Yes. After 8 months, I would recommend bunq to almost any international student arriving in Germany, especially if your passport is one that other neobanks tend to reject. It was easy to set up, the app is genuinely English-friendly and modern, bunq Pro is free for students, my salary and direct debits work without issues, and support has consistently been fast.

The caveats are real but narrow: if you specifically need a true credit line, or you want to buy something on installments through Apple, you will need a second bank for that. And if you want to invest in ETFs, bunq is not the tool for that, a brokerage like Scalable Capital is.

For everyday banking as a student or working student in Germany, bunq has been a genuinely good starting point for me. You can open an account here* and check the current student offer for yourself.

This information is accurate as of June 2026, based on my own account and bunq's published terms. If anything changes, I will come back and update this post.

* Some links on this page are advertising or affiliate links. If you use one and buy or complete an offer, we may earn a commission at no extra cost to you. That support helps us keep improving workingstudentjobs.de, and our reviews and recommendations remain independent.

Frequently Asked Questions

About the author

Dinh Minh (Minton) Vu

Dinh Minh Vu is a software engineer and CS master's student at the University of Passau. As an international student who navigated the German working student system himself, he built workingstudentjobs.de to help other international students find and land Working Student roles in Germany.

Find your next working student job

Browse 1000+ opportunities at top companies across Germany.

Browse jobs