Last checked: June 2026. Bank fees, accepted ID documents, and account-opening rules can change. Always confirm the final conditions on the bank's official website before applying.

Which Bank Account Is Best for Working Students in Germany in 2026?

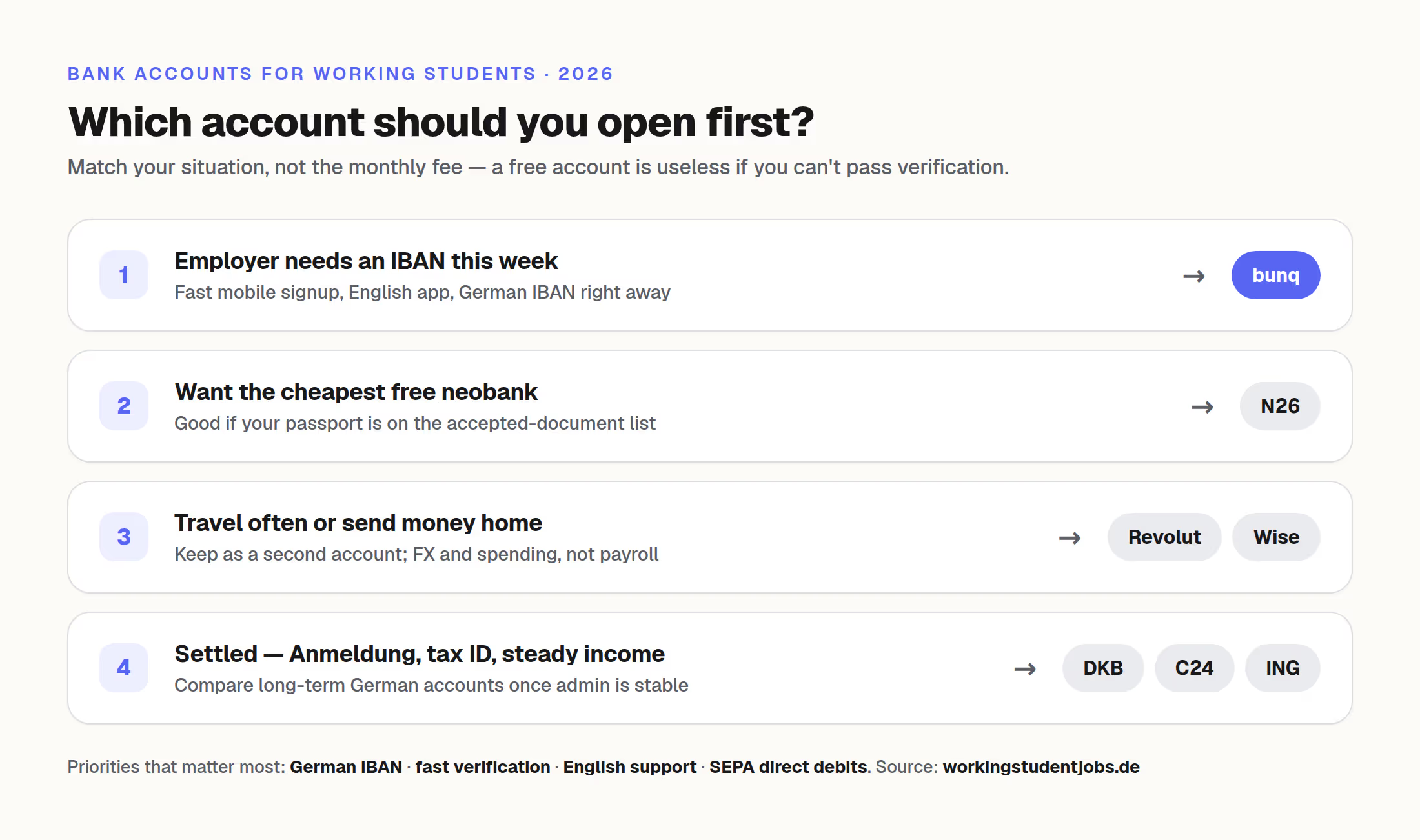

If you need the best bank account for working students in Germany, the short answer is: choose bunq if you need a German IBAN quickly, in English, and before all German paperwork is fully settled. It solves the urgent problem many new arrivals face: your employer asks for an IBAN, and you do not want your first salary payment delayed.

N26 is the strongest free neobank alternative if your passport or residence permit is accepted. Revolut is excellent for travel and multi-currency spending, and German residents may now receive a DE IBAN, but it is still better as a flexible spending account than as the safest first salary account. DKB, C24, ING, and Commerzbank are useful long-term German accounts once you are settled. Wise is great for international transfers, but it is not the best primary German salary account.

I personally use bunq to receive salary in Germany. This guide still compares the main alternatives and points out where bunq is not the best fit, because the right account depends on your passport, residence status, cash needs, and how soon your employer needs your IBAN.

Need a German IBAN fast? Open bunq here* and check the current plan details before signing up.

Quick Verdict: Best Bank Account for Working Students in Germany

For most international working students, the best setup is:

Open bunq first if you need a German IBAN quickly and want English-first mobile banking.

Use N26 instead if you want a free neobank and your identity document is accepted without extra friction.

Use Revolut as a second account for travel, currency exchange, and card spending.

Consider DKB, C24, ING, or Commerzbank later when you have Anmeldung, tax ID, stable income, and a clearer long-term plan in Germany.

The biggest mistake is choosing only by monthly fee. A free account is not helpful if you cannot pass verification or give payroll a usable IBAN before the cutoff.

If you are starting a working student job soon, prioritize:

DE IBAN for salary, rent, tax refunds, and subscriptions

Fast identity verification with documents you actually have

English app/support if you are not comfortable with German banking terms yet

Low monthly cost that still gives you the features you need

SEPA direct debits for rent, health insurance, Deutschlandticket, phone contracts, and utilities

Comparison Table

Bank / account | German IBAN | Monthly fee | Anmeldung / German address friction | English app / support | ID / residence permit caveats | Best for | Main drawback |

|---|---|---|---|---|---|---|---|

Yes, DE IBAN available | bunq Free €0; Core €3.99; Pro €9.99; Elite €18.99; Pro can be free for eligible students (bunq plans*) | Designed for fast mobile signup; no Steuer-ID needed immediately for expats (bunq expats*) | Yes | bunq accepts many EU documents and selected non-EU passports, but some countries need an EU residence permit or are not accepted (bunq ID docs) | Fast German IBAN for international students | Free tier is basic; paid plans cost more unless you qualify for the student discount | |

Yes, DE IBAN | Free; paid plans from €4.90 (N26 pricing) | Mobile signup; must live in a supported country | Yes | N26's document matrix matters: Vietnam, Philippines, and Pakistan are listed as not accepted with passport/ID card, so students from those countries should check residence permit eligibility before relying on N26 (N26 ID docs PDF) | Free German neobank account | ID-document rules can block some non-EU students | |

Often yes for German residents; older/non-migrated accounts may still differ | Standard is free; paid plans available (Revolut plans) | Mobile-first; German residence affects German branch/DE IBAN status | Yes | Revolut says German residents with an IBAN starting with DE are customers of its German branch; check your account details before giving the IBAN to payroll (Revolut Germany fees) | Travel, FX, spending, backup account | Less proven as a first German salary account than bunq/N26 | |

Yes | Free under 28 or with €700 monthly incoming payments; otherwise €4.50 (DKB) | Better once settled; German process and later postal/card steps can take time | Partial | Online opening, but new arrivals may find verification/address requirements less forgiving | Long-term main account | Less beginner-friendly before your first payday | |

Yes | Free Smartkonto (C24 Smart) | German-market app; online opening with smartphone and ID | Mostly German | Requires documents accepted by the German verification flow | Strong free German account after settling | Not as international-student focused as bunq/N26 | |

Yes | Free under 28 or with €1,000 monthly incoming payments; otherwise €4.90 (ING conditions) | Better once you have stable German address/admin | Mostly German | VideoIdent/PostIdent/eID options, depending on eligibility | Established direct bank for long-term use | Higher monthly incoming-payment requirement than DKB | |

Yes | Standard GiroKonto often €4.90 unless conditions are met; StartKonto can be free for younger customers (Commerzbank) | Branch option; more paperwork than neobanks | Partial | Stronger reliance on German documentation and branch/process requirements | Students who want branch support | Slower, less convenient for urgent IBAN needs | |

Usually Belgian EUR IBAN, not DE | Account often free; fees apply by use | Easy international setup | Yes | Wise EUR details are generally Belgium-based for Europe (Wise account details*) | Sending money home, receiving foreign currency | Not ideal as primary German salary/rent account |

Ready to open your account? Open bunq free* · Open Wise*

Do you need a blocked account (Sperrkonto)?

If you are an international student from outside the EU, you may need to prove funds before getting a German student visa — and that means opening a blocked account (Sperrkonto) first.

Who needs a Sperrkonto:

Non-EU/EEA students applying for a German student visa must show €11,904 (2026 figure) deposited in an approved blocked account. The money is released as roughly €992 per month once you arrive.

EU and EEA students, and German residents, do not need a Sperrkonto — they go straight to a regular Girokonto (current account).

How to decide:

International non-EU student arriving in Germany → open a Sperrkonto first, then open a Girokonto after arrival.

EU/EEA student or German resident → skip the Sperrkonto, open a Girokonto directly.

Expatrio is one of the most straightforward options for a Sperrkonto with a fast online process and English support. For a full breakdown of how the blocked account works, which providers to use, and common mistakes to avoid, see our blocked account Germany guide.

Open a blocked account with Expatrio*

How We Ranked the Accounts

This article is written for working students, not for people optimizing credit cards or investing. A working student account has to solve practical problems fast:

Can your employer pay your salary to it without HR friction?

Can you open it with your current documents?

Can you use it before or shortly after Anmeldung?

Can you understand the app and support flow in English?

Can you set up SEPA direct debits for rent, health insurance, phone, and public transport?

Will the account still make sense after your first semester or first job?

That is why bunq ranks first for many new international students even though N26 has a free Standard account. Price matters, but the real cost of the wrong account is delayed salary, failed verification, and rejected direct debits.

Why Working Students Need the Right Account Before Payday

Your employer needs an IBAN for payroll, usually before the first payroll cutoff. If you start in the middle of the month and give HR your bank details late, your first salary can be pushed to the next pay cycle.

Technically, a German employer should be able to send SEPA payments to an IBAN from another EU/EEA country. The European Commission describes "IBAN discrimination" as being unable to make or receive a SEPA transfer or direct debit from an account in another member state (European Commission). In practice, however, some payroll systems, landlords, utility providers, and subscription flows still create friction when the IBAN does not start with DE.

That is why a German IBAN is operationally useful. It reduces edge cases.

You will likely use the account for salary, rent, health insurance, Deutschlandticket, phone contracts, tax refunds, and SEPA subscriptions.

If you are still comparing salaries, use the Working Student Salary Guide and the Working Student Tax Calculator to estimate how much should arrive in your account after deductions. For social security and tax rules, read the working student tax guide.

Best Overall: bunq

bunq is the best overall bank account for international working students in Germany who want speed, English support, and a German IBAN without waiting for the traditional German banking process.

The main reason is simple: bunq is built around mobile onboarding for international users. You sign up from your phone, verify your identity, and can create a German IBAN from the app. bunq's official plan comparison says German IBAN creation is included, and its expat page positions the account for people who are new to Germany and do not yet have every local document ready.

For working students, this matters more than small differences in card perks. If your employer asks for bank details today, a fast DE IBAN is more valuable than a perfect account that takes a week or more to activate.

Why bunq works well for working students

German IBAN: helpful for salary, rent, tax refunds, and direct debits.

English-first app: less confusion when you are new to German financial terms.

Fast mobile setup: useful before your first payday.

Multiple account options: bunq Free covers basics; Core, Pro, and Elite add more features. Eligible students can get bunq Pro free.

International positioning: stronger fit for expats and non-German speakers than many traditional banks.

Where bunq is not perfect

bunq is not automatically the cheapest account if you want features beyond the free tier. In June 2026, public pricing lists bunq Free at €0/month, Core at €3.99/month, Pro at €9.99/month, and Elite at €18.99/month. However, bunq's student discount can make Pro free for eligible university students in Germany who are 25 or under and upload a valid proof of enrollment, such as an Immatrikulationsbescheinigung, student ID card, or university confirmation letter (bunq student discount*).

If you do not qualify for the student discount and only care about a free account, N26 Standard may be cheaper if your documents are accepted.

You should also check bunq's accepted ID document list before assuming your passport is enough. bunq accepts passports from many non-EU countries, including Vietnam, but some countries are not accepted or require a European residence permit. This is still often smoother than traditional banks, but it is not universal.

Who should choose bunq?

Choose bunq if you need a DE IBAN quickly, want an English app, do not want to wait for branch appointments, and are still sorting out Anmeldung, tax ID, or housing.

Do not choose bunq only because of this affiliate link. Choose it if the speed, German IBAN, and international-student fit solve your actual problem.

If that is your situation, open bunq here* and verify the current plan and ID requirements before completing signup.

Best Free Alternative: N26

N26 is the best free alternative for students who want a simple German neobank account and whose identity documents are accepted. N26 Standard is free, with no account-opening fee, no monthly account-management fee, no minimum deposit, and no minimum monthly incoming payment according to N26's account comparison page.

N26 also confirms that you can give your N26 IBAN to your employer for salary payments. For many EU students and many non-EU students with accepted documents, it is a strong choice.

The reason N26 is not automatically the top recommendation for every international student is the document matrix. N26 publishes a country-by-country list of accepted ID documents for Europe in its official accepted documents PDF. In that PDF, some nationalities cannot verify with passport or ID card alone. For example, Vietnam, the Philippines, and Pakistan are listed with "No" for passport and "No" for ID card. Residence permits are only available as a verification document for selected nationalities and must meet N26's requirements.

This does not mean N26 is bad. It means you should not make N26 your only plan until you check your nationality and document type.

Choose N26 if your nationality/document combination is accepted, you want a free German IBAN, and you are comfortable with a fully digital bank. Use bunq instead if N26's ID-document requirements create uncertainty and your employer needs bank details soon.

Best for Travel and Multi-Currency: Revolut

Revolut is excellent as a travel and spending account. If you send money home, travel in Europe, pay in other currencies, or want card controls, Revolut is often the most flexible account in your wallet.

The important 2026 update: Revolut is no longer simply a Lithuanian-IBAN option for Germany. Its German fee document says German residents with a DE IBAN are customers of Revolut Bank UAB, German Branch. Some older or non-migrated accounts may still not have a DE IBAN.

The practical rule: if your Revolut account shows a DE IBAN, it may work for salary. If it shows a non-DE IBAN, ask HR first. Even with a DE IBAN, many students still prefer bunq or N26 as the primary salary account and Revolut as a secondary spending account.

Revolut Standard is free. Paid plans add travel, insurance, cashback, and exchange features depending on the plan. Choose Revolut if you travel often, exchange currencies, send money internationally, or want a second card for budgeting.

Do not rely on Revolut as your only German account until you have checked your exact IBAN and confirmed your employer accepts it.

For international transfers, Wise* consistently beats Revolut on mid-market rate and fee transparency.

Best Long-Term German Accounts: DKB, C24, ING, Commerzbank

Once you are settled in Germany, the best account may be a more traditional German current account. These options are not always fastest in your first week, but they can be excellent long-term.

DKB

DKB is one of the strongest long-term online banks in Germany. The account is free for customers under 28 or with at least €700 monthly incoming payments, which many working student salaries can clear.

The downside is onboarding friction. DKB can be a great second account once your address, tax ID, and German admin are stable, but it is less ideal if you need an IBAN today.

Choose DKB later if you want a strong German direct bank with free-account conditions that fit student income.

C24

C24 Smart is a strong free German account with Mastercard, girocard, sub-accounts with IBANs, budgeting features, and a modern app.

For international working students, the limitation is language and target audience. If you are comfortable with German and already have your local documents sorted, C24 can be very good. If you need English onboarding and your first salary IBAN urgently, bunq or N26 is usually easier.

ING

ING is a well-known German direct bank. Its Girokonto is free if you are under 28 or receive at least €1,000 monthly incoming payments; otherwise it costs €4.90/month.

The €1,000 income threshold can be fine if you work enough hours, but not every student reaches it every month.

Commerzbank

Commerzbank is useful if you want physical branch support, in-person help, or a traditional German bank.

But for a new international student who needs an IBAN before payday, Commerzbank is usually slower than a mobile bank. Also be careful with pricing: the regular GiroKonto and youth/student-style offers are not the same.

Choose Commerzbank if you want branch support and do not need the fastest account opening.

Where Wise Fits

Wise is useful, but it is not the best primary bank account for working students in Germany.

Use Wise for sending money home, receiving other currencies, transparent currency conversion, and international transfers.

Do not rely on Wise as your only German salary account if your employer expects a DE IBAN. Wise's EUR account details for Europe are typically Belgium-based rather than German, so the same practical friction can apply with HR systems, landlords, direct debit forms, and subscriptions.

For the detailed salary-account comparison, read bunq vs Wise Germany: which works for your Werkstudent salary?.

The best setup for many international students is:

bunq or N26 for German salary and direct debits

Revolut or Wise* for travel, currency exchange, and international transfers

Can Your Employer Pay to a Non-German IBAN?

In principle, yes, if the account is a valid SEPA account. In practice, maybe.

EU rules are meant to prevent IBAN discrimination inside SEPA. If a company refuses a valid EU IBAN only because it comes from another member state, that can be a compliance issue.

But when you are starting a working student job, you may not want to turn your first payroll conversation into a legal argument. You want to get paid on time.

That is why a DE IBAN is the low-friction option. It avoids unnecessary back-and-forth with payroll, landlords, public transport subscriptions, phone contracts, health insurance direct debits, and tax refunds.

If you already have a non-German IBAN, ask HR early: "Can payroll pay salary to this SEPA IBAN?" If the answer is unclear, open a German IBAN account before the cutoff.

What If You Do Not Have Anmeldung Yet?

Anmeldung is your official address registration in Germany. You often need it for traditional banking, tax, and public administration. The problem is timing: appointments can take time, while your employer may ask for an IBAN immediately.

If you do not have Anmeldung yet:

Try a mobile-first bank built for international users, such as bunq.

Check whether N26 accepts your nationality and ID document.

Avoid relying on a traditional branch bank if your first salary is due soon.

Update your bank profile later once you receive your address registration and tax ID.

Do not lie about your address or tax status. If a bank asks for a document you do not have, choose a bank whose onboarding matches your situation.

What If N26 Asks for a Residence Permit?

This is common for some non-EU students. N26's accepted-documents PDF is not just a formality. It can determine whether you can open the account at all.

For example, the June 2026 N26 document matrix lists Vietnam, the Philippines, and Pakistan with "No" for passport and "No" for ID card. That means students from these countries should not assume a passport alone will work. Residence permit verification is also limited to selected nationalities and must follow N26's requirements.

If N26 is uncertain for your nationality, check N26's official PDF, compare bunq's accepted ID document page, prepare your electronic residence permit if you already have it, and do not wait until your employer's payroll deadline.

This is why the best account for international students is not always the cheapest account.

Should You Use bunq, N26, or Revolut for Salary?

Use bunq for salary if you want the fastest international-student-friendly route to a German IBAN and you value English onboarding.

Use N26 for salary if your document combination is accepted and you want a free German neobank.

Use Revolut for salary only after checking that your account has a DE IBAN and your employer accepts it.

If you are unsure, the most practical setup is:

Primary salary account: bunq or N26

Daily spending/travel account: Revolut

International transfers: Wise* or Revolut

Long-term German account later: DKB, C24, ING, or Commerzbank

Documents Checklist for International Students

Before applying, prepare your valid passport or national ID card, residence permit/eID if you already have it, address details, smartphone with working camera, German phone number if available, enrollment certificate for student offers, and tax ID once you receive it after Anmeldung.

For a working student job, your employer may also ask for your IBAN, tax ID, health insurance membership certificate, social security number if already issued, and enrollment certificate.

The bank account is only one part of the admin setup, but it directly affects whether your salary arrives on time.

Decision Guide by Situation

"I just arrived and my employer needs an IBAN this week." Choose bunq first. It is the strongest fit for fast setup, English app, and DE IBAN access.

"I want the cheapest possible German neobank." Try N26 Standard, but check the accepted-document matrix before relying on it.

"I am from Vietnam, the Philippines, Pakistan, or another country with stricter N26 verification." Do not assume N26 will work with your passport. Check N26 and bunq ID rules before your payroll deadline.

"I travel often or send money home." Use Revolut or Wise* as a secondary account. Keep a German IBAN account for salary and direct debits.

"I already have Anmeldung, tax ID, and stable monthly income." Compare DKB, C24, ING, and Commerzbank. They may be better long-term than a neobank-only setup.

"I mostly need a bank account for a Werkstudent job." Prioritize DE IBAN, fast verification, low monthly fees, and easy SEPA direct debits over premium card features.

Final Recommendation

If you are an international working student in Germany and need a bank account before your first paycheck, start with the account that removes the most friction: a German IBAN, fast verification, English app, and low setup effort.

For that use case, bunq is the strongest overall recommendation. N26 is a good free alternative if your documents are accepted. Revolut and Wise are excellent secondary tools for travel and international money movement. DKB, C24, ING, and Commerzbank become more attractive once your Anmeldung, tax ID, and income pattern are stable.

Ready to set up your salary account? Open bunq here* and confirm the latest plan, document, and fee details before applying.

* Some links on this page are advertising or affiliate links. If you use one and buy or complete an offer, we may earn a commission at no extra cost to you. That support helps us keep improving workingstudentjobs.de, and our reviews and recommendations remain independent.

Frequently Asked Questions

About the author

Dinh Minh (Minton) Vu

Dinh Minh Vu is a software engineer and CS master's student at the University of Passau. As an international student who navigated the German working student system himself, he built workingstudentjobs.de to help other international students find and land Working Student roles in Germany.

Find your next working student job

Browse 1000+ opportunities at top companies across Germany.

Browse jobs